The End of Development

The End of Development

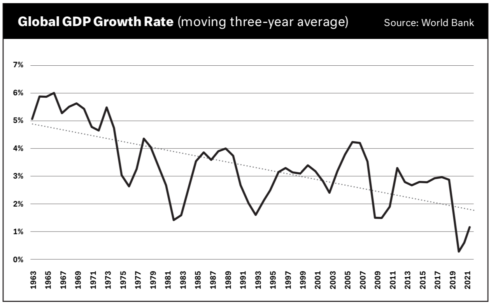

Discussion in the United States about secular stagnation, a long-term tendency toward weak business investment and slow growth, has mostly focused on wealthy countries. But slowing growth around the world cannot be explained as the sign of economic “maturity.”

When I was in high school, my economics class read The End of Poverty by Jeffrey Sachs. The book is a passionate appeal to help those living in the worst poverty in the world. Sachs writes that we should not worry too much about the people in second-to-last place, such as the poorly paid workers in labor-intensive industries who were then the focus of considerable debate and activism on U.S. college campuses. Sweatshop workers, Sachs conceded, were on the bottom rung of the ladder. But subsistence farmers were not on the ladder at all. Once we helped them get a foothold, they could begin ascending from textiles all the way up to high tech. I internalized Sachs’s argument, sensing it would help me feel better about the world we live in.

This idea that sweatshops are good is so convenient that it will probably live forever. It provided the basic logic behind Matthew Yglesias’s defense of unsafe workplaces published after more than 1,100 people died in the 2013 Rana Plaza factory collapse. Safety is nice but “money is also good,” and who could deny that “Bangladesh has gotten a lot richer” in recent decades? History might be a slaughter bench, but at least it had a clear direction, namely the upward sloping trend of GDP per capita. Vox, cofounded by Yglesias in 2014, ran similar takes, including the charge that Bernie Sanders’s “war on trade” “would hurt the very poorest people on Earth” by depriving them of low-wage employment in export industries. So it was striking when Yglesias took note of a new trend “in which countries start to lose their manufacturing jobs without getting rich first.” Disturbingly, this was not because of protectionism or misguided safety regulations but because of dynamics internal to capitalist development. “Structural change,” he wrote, “is moving in the wrong direction.” The ladder was broken.

Since 2013, there has been increasing discussion in the United States about secular stagnation, a long-term tendency toward weak business investment and slow growth. The conversation is often centered on wealthy countries, which makes it possible to imagine that we’ve become so rich that we’re sated with physical products and naturally spend more and more of our income on services and experiences. Thus, the titles of recent books: Dietrich Vollrath’s Fully Grown: Why a Stagnant Economy Is a Sign of Success, or Tyler Cowen’s The Great Stagnation: How America Ate All the Low-Hanging Fruit of Modern History, Got Sick, and Will (Eventually) Feel Better.

These reassurances look glib when confronted with global economic stagnation. Slowing growth around the world cannot be explained as the sign of economic “maturity.” Instead, many countries are experiencing “premature deindustrialization,” a term coined by José Gabriel Palma and popularized by Harvard economist Dani Rodrik. Earlier processes of deindustrialization left rust belts across the poorer parts of rich countries, from Kenosha to Osaka. It is usually assumed that the old factory jobs moved to other countries. Rodrik’s observation is that deindustrialization has been happening across the Global South as well, where industrial employment has already peaked and begun to decline. This is “premature” in the sense that the peaks are coming at a lower level (measured in share of employment and output or the level of national income) than they did in the now-rich countries that industrialized earlier. At the height of the golden age of capitalism in 1973, Japan, Germany, and the UK had roughly 40 to 50 percent of their populations working in manufacturing. In Brazil, by contrast, the peak, reached in 1986, was 23 percent; for Nigeria, in 1991, it was just 13 percent.

It is easy, and appropriate, to be skeptical of the common attitude that good jobs are necessarily manufacturing jobs. There are a wide range of valuable economic activities, and there is no historical necessity that makes some kinds of jobs worse than others. Anyway, plenty of workers hated (and still hate) their manufacturing jobs. The trouble is that it is hard to find successful examples of alternative development models. As economic historian Robert Allen has pointed out, countries that are rich today were generally rich in 1820. Among large countries, the exceptions are Russia, Japan, South Korea, Taiwan, and China. In addition to radical and unpleasant institutional transformations (whether socialist revolution or Japanese colonialism), these countries all underwent industry-led growth. Manufacturing was just as important elsewhere, even when the project remained incomplete: per capita income in Latin America doubled between 1950 and 1980, the years of import-substitution industrialization. It is this historical reality, not just nostalgia, that leads people all over the world to vote for politicians promising to bring back smokestacks and steel.

There is limited understanding of the causes of secular stagnation on a global scale. We can distinguish between explanations focused on demand and those focused on supply. From one perspective, stagnation is the result of weak effective demand for goods and services, and an improvement in the demand outlook would mean an escape from stagnation. From the other, even a restoration of aggregate demand would run aground on deeper global economic structures, specifically a lack of new industries that could expand production and employment in response to a new business upswing.

There can be little doubt that global demand is weak. Even before COVID-19, what existed of a post-2008 expansion was over. The Financial Times reported in 2019 that the “global economy has entered a period of ‘synchronised stagnation’ with weak growth in some countries and no growth or a mild contraction in others.”

This sort of global demand deficiency has fed dreams of global demand management since the Keynesian revolution in economics. A 1949 UN report, largely written by Keynes’s follower Nicholas Kaldor, called for an automatic countercyclical program of foreign investment, to be administered by the World Bank and funded by the industrial nations. The report was rejected by the United States, which then accounted for half of the world’s industrial production, and went nowhere. But the problem did not go away.

NSC-68, the famous State Department planning document prepared in 1950, predicted that the entire “free world” would soon suffer a “decline in economic activity of serious proportions unless more positive governmental programs are developed than are now available.” Fortuitously, U.S. rearmament soon provided a massive global stimulus (as well as the dollars needed to lubricate foreign exchange). Total U.S. military spending during the Korean War exceeded $1 trillion (inflation adjusted), an amount six times larger than the celebrated Marshall Plan. In 1953, the value of total exports in the world economy was 40 percent higher than it had been four years before. While military spending was far from the only force buoying aggregate demand during the heyday of the liberal international order, its importance underlines the ad-hoc nature of global economic management in a period supposedly more open than our own to government planning.

The problem of global demand resurfaced in the 1970s. At first, the problem was too much demand. International business cycles became increasingly synchronized, and during the upswing unbearable pressure was placed on basic commodity prices (most famously, but not exclusively, oil). Then, global crash: between 1974 and 1975, industrial production in the advanced capitalist countries fell by 10 percent and international trade by 13 percent. The U.S. government budget deficit initially played its traditional role in keeping the bottom from falling out under global aggregate demand. But as the U.S. recovery gathered strength, so did the trade deficit and inflation, raising fears of a run on the dollar. Further global stimulus would have to come from nations with a trade surplus—principally Germany and Japan. In 1978, the G7 officially agreed to pursue coordinated stimulus, but Germany—the appointed “locomotive” of demand—was not seriously interested in the project. In 1979, German pressure helped Federal Reserve chair Paul Volcker push U.S. policy in an extremely restrictive direction, a move that triggered worldwide depression and debt crises across the Global South.

The global demand contractions of the 1970s and 1980s halted industrial expansion in many parts of the world. In the wealthy countries of the OECD, the manufacturing share of employment (and in many Western European countries, the absolute number of jobs) peaked around 1974. In the United States, relative decline had begun after the Korean War, but absolute decline set in after 1979. In the “lost decade” of the 1980s, manufacturing employment also fell in sub-Saharan Africa and stagnated in Latin America. The decline of industry was matched by the growth of finance, and it is through these channels that the more recent globally coordinated crisis response has occurred. During the 2008 crash, as Adam Tooze has emphasized, the Federal Reserve administered liquidity to foreign central banks through dollar swap lines—“an act of international . . . stabilization a good deal larger than the Marshall Plan.” Like domestic quantitative easing, these interventions prevented a downward spiral of debt defaults but failed to restore satisfactory levels of business investment. Globally as domestically, there are limits to even the most extraordinary monetary policy.

Recent experience shows that the movement of demand can have highly consequential effects on political events and social life. Slowing demand from the United States, the European Union, and China contributed significantly to a sharp fall in commodity prices between 2011 and 2014. The results included a financial crisis in Russia and Brazil’s worst recession since the 1930s (which brought the fall of Dilma Rousseff’s Workers’ Party and the rise of Jair Bolsonaro). The emerging markets slump in turn contributed to a sectoral slowdown in the U.S. capital goods industry. The heavy equipment manufacturer Caterpillar (which gets more than half of its revenue from foreign sales) saw a 30 percent decline in revenue between 2014 and 2016. As Neil Irwin has argued, this caused a noticeable uptick in unemployment in precisely those manufacturing-dependent areas that won Donald Trump the 2016 election. While the limits of international stimulus, much less methods for stabilizing commodity prices, remain a matter of speculation, the 2011–2016 sequence reminds us that our political fates remain linked by the movement of global demand.

But even if the political difficulties of global stimulus can be overcome, what form would growth take? Perhaps the world economy is simply saturated with the industries that distinguished export-led growth—textiles, apparel, footwear, steel, autos, basic electronics. The persistent overcapacity theory is often associated with the Marxist economic historian Robert Brenner, but the anxiety also surfaces in the business press and among mainstream economists. Since 2016, the OECD has convened a Global Forum on Steel Excess Capacity, which issues regular updates on the steady growth of excess capacity (700 million metric tons in 2020). Its reports describe steel as “a driver of industrialization” but insist that “increases of capacity should be purely based on market forces,” ruling out “market-distorting subsidies” (of the sort that now-dominant steelmakers relied upon to attain their position). This is a clear message to developing nations that the driver of industrialization is not going to pick them up.

Any economics student can tell you that after manufacturing comes services. Could they be a new engine of growth? Just as workers in rich countries have moved from factories to cubicles and hospital rooms, could prematurely deindustrialized countries climb the ladder through non-tangibles? The idea of services-led growth might have originated with a 1981 paper by Werner Baer and Larry Samuelson, who noted the obvious “failure of industrialization to create enough employment to effectively absorb the urban masses swelled by rural-urban migration and population growth.” In 1984, Jagdish Bhagwati bemoaned the fact that immigration restrictions stood in the way of truly global competition for service jobs, but looked to the development of “disembodied” services to take the place of physical migration. In the 1990s, the development of information technology began to make this look more feasible.

The lodestar of service-led growth is India, where businesses have managed to turn information and communication services (think of the famous call centers) into a tradable export. Between 1950 and 2009, the share of agriculture in India’s GDP fell from 55 percent to 17 percent. At the same time, industry increased its share but remained under 30 percent. It was services that dominated the Indian economy by 2009, at 57 percent of GDP. Despite talk of a service “sector,” the category contains incoherent multitudes: barbers and bodyguards, custodians and consultants. It was only a specific subset—communications, business, and financial services—that replaced industry as the driver of India’s growth in the 1990s and 2000s. But even those economists who take a bullish position on this development path have their doubts. Barry Eichengreen and Poonam Gupta, for example, proclaim the “good news” that “it is no longer obvious . . . that manufacturing is the main destination for the vast majority of Indian labor moving into the modern sector.” But they also describe “employment in modern services” only as “a useful supplement to employment in manufacturing as a route out of rural poverty” (emphasis added).

Rwanda, which averaged over 8 percent annual economic growth from 1995 to 2015, has also been offered as an example of service-led growth. A major component of the country’s “service exports” is tourism, which is said to have grown over 20 percent per year between 2002 and 2012. As with India, even proponents of the service strategy give reason for skepticism. In this case, “The main driver of tourism, gorilla trekking, is reaching full capacity,” economists Ggombe Kasim Munyegera and Richard S. Newfarmer wrote in 2018, “and the country needs to develop additional attractions to keep the sector growing.” Even if these attractions materialize, which one hopes they will, it is important to remember we are talking about growth from a very low baseline. In terms of purchasing power–adjusted GDP per capita, Rwanda ranks 166th in the world. There is no evidence here of a way for poor countries to become middle-income countries.

The major problem with services is that they are not susceptible to the kinds of productivity increases that characterize industrial processes. According to the OECD, labor productivity in member states is 40 percent lower in nongovernment services than in manufacturing; over the past thirty years, labor productivity has grown more than twice as fast in manufacturing as in services. The growing share of service employment, in rich and poor countries alike, thus represents a transfer of labor to low-productivity sectors, and therefore a decline in overall growth rates. (This is the reverse of the path of successful industrializers, who moved their populations out of low-productivity farming and into high-productivity industry.)

It’s possible that services, or at least some important subset of that broad category, have more growth potential than we have so far predicted. But we remain short on examples. Just as problematically, there is evidence that services that do display productivity gains cannot absorb enough labor to compensate for the loss of other ways of making a living. For a time, manufacturing was capable of both becoming more productive than farming and absorbing a larger relative share of the population. This double advantage so far eludes the services.

Given the apparent advantages of industry, we might also ask whether the premature deindustrialization diagnosis is overstated. Hasn’t China, well on its way to becoming the world’s largest economy, seen fantastic manufacturing-led growth in this century? But even the youngest industrial giant is showing signs of maturity. Before 2008, an estimated 75 percent of China’s industries suffered excess capacity. Still, while the rest of the world contracted and demands for Chinese exports collapsed, China maintained annual growth rates between 9 and 10 percent from 2008 to 2010. This stability was purchased with a massive stimulus several times as large (compared to GDP) as the U.S. response. Unlike in the United States, investment in China is not held back by the requirement that it produce private profits. But even unencumbered by this requirement, Chinese officials find they have run out of outlets for public investment: “We have plenty of bridges and roads already,” an official from Sichuan Development, a state-owned enterprise, told the Financial Times in 2019. Over the last decade, Chinese manufacturing has also declined as a share of employment and value added.

There has been pushback against the premature deindustrialization thesis from other parts of the world, too. According to Jim Yong Kim, president of the World Bank from 2012 to 2019, “There’s not a single African head of state that I’ve seen in the last two years who doesn’t tell me that ‘we’re preparing for industrialization.’” Kim is skeptical; a recent publication by Christopher Cramer, John Sender, and Arkebe Oqubay, African Economic Development, tries to answer his doubts. The authors write in the broadly left-wing structuralist tradition, against neoclassical growth theory and the Washington Consensus. They argue that it is not self-evident what the “industry” in (de)industrialization should mean, or that its meaning should remain the same throughout history. The clearest example the book offers of this rethinking is the “industrialization of freshness,” a trend toward specialized export agriculture that both generates a competitive tradable good and shows potential for absorbing labor and productive investment. They propose “a large-scale investment in Ethiopia promoting a rapid expansion in high-quality, premium-priced, wet-processed coffee production capacity,” including state-funded investment in infrastructure and electrification. But even as Ethiopia’s industrial sector (examined in greater detail in this issue by Anakwa Dwamena) is expanding output and increasing its share of the country’s GDP, manufacturing employment as a share of overall employment has been stagnant.

What if societies organized production around basic domestic needs instead of export-led growth? Larry Summers, expressing characteristically belated second thoughts, has suggested that the world “move from a just-in-time world to a just-in-case world.” “Just-in-time” here refers to the lean style of logistics management originally associated with Japanese manufacturing. In this model, no spare parts are left lying around; everything arrives from the upstream supplier right when it’s needed. Shifting to “just-in-case” would go against the logic of efficiency maximization, building in redundancy so that during a pandemic, for example, it would be possible to increase production of necessary medical equipment in time to save lives.

If efficiency (as it has been defined by market competition) is not in control, who or what is? The possibility of “industrial policy” has been raised by a number of economists, including the authors of an International Monetary Fund (IMF) white paper titled, “The Return of the Policy That Shall Not Be Named.” Yet it seems quite likely that, after the pandemic recedes, business opinion will either forget about industrial policy or rediscover its objections. Already, editorials in Bloomberg and the Financial Times have criticized Biden’s proposed “Buy American” provisions: “A judicious shift from ‘just in time’ to ‘just in case’ is required,” but “suppressing trade would raise costs and impair competitiveness, leaving everyone worse off.” There is still immediate hostility toward any weakening of the link between investment and profitability criteria. Also telling is Bloomberg’s direct address to its readers: “Companies, for their part, should reflect on the past year’s experience and do a better job of mapping and managing their supply chains. . . . They shouldn’t need governments to direct this work.” If this is the elite attitude toward U.S. industrial policy, one can only imagine the reception for industrial policy in poorer countries that departs from capitalist logics. And if it doesn’t depart from them, why expect anything from the policy in the first place?

In a June 1933 lecture, John Maynard Keynes embraced domestic-oriented strategies: “let goods be homespun whenever it is reasonably and conveniently possible, and, above all, let finance be primarily national.” In The General Theory of Employment, Interest and Money, Keynes looked forward to the day when trade would stop being “a desperate expedient to maintain employment at home by forcing sales on foreign markets and restricting purchases” and become “a willing and unimpeded exchange of goods and services in conditions of mutual advantage.” More recently, Amit Bhaduri has argued for developing countries to “shift from the external to the internal market so as to ensure that the poor majority of our population participates in the growth process both as consumers and as producers.” While “nobody has a clear idea” what a humane growth model would look like, Bhaduri writes, the alternative would need to be democratic: both more decentralized than the usually authoritarian state-led growth of the 1950s–1970s, and independent of existing political parties whose links with multinational corporations are too strong to be broken from within. The rest would emerge, if at all, from the unforeseeable interactions of an “enormous diversity of people’s resistance and local initiatives for development.”

For any of this to work, states would need to be able to apply capital controls as needed. As the economist James Crotty has insisted, Keynes was deeply convinced that “central control of capital movements, both inward and outward, should be a permanent feature” of the international economy. The ability of capital to circulate globally in search of higher returns threatens every experiment in political control of the economy. But since the 1970s, capital controls have been deeply disfavored by anyone with any power. One of the few dissenters, ex-IMF economist Olivier Blanchard, drew out the implications in a memorable tweet in 2018: “Could it be that, given the political constraints on redistribution and the constraints from capital mobility, we may just not be able to alleviate inequality and insecurity enough to prevent populism and revolutions. What comes after capitalism?” For Blanchard, it is easier to imagine the end of capitalism than the restriction of capital mobility.

The counterpart to the inability to imagine a future is fixation on the past, or rather an ideal image of the past buffed until it looks like a bright future. Take Harvard Business School professor Rebecca Henderson, author of the urgently titled 2020 book Reimagining Capitalism in a World on Fire. She reports that a friend told her she “should’ve called it Rediscovering the Capitalism We Had in the ’50s and ’60s, Only Without the Misogyny and the Racism.” Henderson basically agreed with her friend, objecting only that “that’s not a great book title, and that’s one hell of an asterisk.” A policy essay issued by the “liberaltarian” Niskanen Center similarly blames our political problems on the failure of today’s business elite to live up to the example of “the corporate officials of the postwar era [who] felt a sense of responsibility for the well-being of the larger society.”

The postwar order so widely mourned today was dominated by men who had a clear vision of how the world economy ought to run. This vision was crystallized by economist and Kennedy adviser Walt Rostow, who stylized the experience of the English industrial revolution into a recipe any country could repeat. In 1961, Rostow predicted that the following countries would achieve “self-sustaining growth by 1970”: Argentina, Brazil, Colombia, Venezuela, India, the Philippines, Taiwan, Turkey, Greece, and “possibly” Egypt, Pakistan, Iran, and Iraq. The failure of this developmental model in the 1970s opened the door for neoliberal development, whose failure in turn has generated the current impasse. Without an explanation of how this all went wrong, nostalgia for the postwar era offers nothing to today’s debates.

Capitalism’s publicists are experiencing something of what Marxists went through after 1989, with one important difference: capitalism may be increasingly discredited, but it has not disappeared the way state socialism did. If an optimistic scenario is hard to imagine, it is easy to imagine a future: the continued dominance of limitless private accumulation in a world of slowing growth, frenetic financial markets, and border walls. Those admirers of capitalism who still hold out for something rosier can take lessons from the post-1989 experience of the left: disavow mechanical stage-ism, keep an eye out for small but promising local developments, and remember that rival ideologies have weaknesses just like your own does. Your critics are overconfident when they tell you there is no alternative to global stagnation. History is full of unexpected turns and almost anything is possible. But as leftists have long known, mere possibility is a limited consolation. It sure would be nice to have some idea where you’re going.

Tim Barker is a historian of modern American capitalism and a member of Dissent’s editorial board.