Fatter Cats: Executive Pay and American Inequality

Fatter Cats: Executive Pay and American Inequality

Between 1965 and 2000, CEO compensation grew by about 2500 percent, while worker compensation inched up only about 30 percent. This is a market malfunction, a democratic disaster, and a key driver of inequality, as the political currents that eroded the bargaining power of ordinary Americans have also buoyed the incentive and the opportunity of the richest 1 percent to pad their incomes.

This series is adapted from Growing Apart: A Political History of American Inequality, a resource developed for the Project on Inequality and the Common Good at the Institute for Policy Studies and inequality.org. It is presented in nine parts. The introduction laid out the basic dimensions of American inequality and examined some of the usual explanatory suspects. The political explanation for American inequality is developed through chapters looking in turn at labor relations, the minimum wage and labor standards, job-based benefits, social policy, taxes, financialization, executive pay, and macroeconomic policy. Previous installments in this series can be found here.

Executive pay has risen dramatically—both in absolute terms and in relation to median wages—across the last generation. The spike in executive salaries is both a key driver of inequality at the top end of the income spectrum (about half of the “1 percent” are executives or managers at non-financial firms) and a symbolic marker of social norms in our “winner-take-all” economy.

Conservative economists have tried to spin this as a triumph of market forces, manifesting the ability of superstar innovators to pull away from the pack in a global, wired economy. But there is little evidence to sustain this view. Gains in executive pay have dramatically outstripped gains in educational attainment and bear little relation to merit or productivity, as the CEOs of successful and failed enterprises alike have made off like bandits. Instead, the trajectory of CEO pay is a political story, embedded in tax policy and in the slow collapse of meaningful corporate regulation or governance.

A Short History of Executive Pay

There has always been a strong populist distaste for the overcompensation of business leaders, both for the sheer injustice of the inequality it fosters and for its political implications. “To base a state with glaring social inequalities on political institutions where people are supposed to be equal,” as Henry George famously observed, “is to stand a pyramid on its head. Eventually, it will fall.” In many respects, the debate today echoes that of a century ago. Some saw the accumulation of wealth in strictly market or “social Darwinist” terms, while others—as the muckraking moniker “robber barons” suggests—saw it as little more than theft.

In the early-twentieth-century United States, as state regulation of the market expanded, this became a political and a policy issue. Federal officials questioned the lavish compensation of railroad executives, for example, in the wake of government’s takeover of the industry during World War I. The onset of the Great Depression both focused the nation’s attention on the contrast between executive compensation and general privation and expanded the jurisdiction of federal agencies regulating business activity. The most important of these for the subsequent history of CEO pay was the establishment of the Securities and Exchange Commission (SEC) in 1934. A key element of this new regulatory oversight over stock and securities trading was regular accounting disclosure—including that of executive salaries—by listed firms.

For most of the middle years of the last century, executive salaries (especially by contemporary standards) were relatively modest. Second World War–era wage and price controls substantially narrowed the gap between executive and average pay, and a progressive tax structure kept a lid on wage growth at the top end after the war—part of the “great contraction” of midcentury wage and income gaps. Indeed, it took more than a quarter of a century for executive pay to rebound to prewar levels.

The slow rise in executive pay during the heyday of postwar growth would seem to undermine the assumption that executive pay is simply a reward for strong economic performance. Indeed patterns of compensation seemed most responsive not to corporate success (measured by profits or stock value) but to changes in tax policy. The high marginal income tax rates of the 1940s and 1950s meant that only substantial raises would have much effect on after-tax compensation. This not only discouraged such commitments but pressed firms to look for alternatives.

The tide began to turn, however, with the Revenue Act of 1950, which opened the door for “qualified” stock options. Since these were not taxed as income, and any appreciation in stock value was taxed at the lower capital gains rate, they became a preferred method of boosting CEO pay. Not surprisingly, the composition of executive pay shifted back toward salaries when subsequent reforms (1964, 1969) narrowed the gap between income and capital gains rates. In the 1980s and ‘90s, both forms of executive pay took off as marginal income tax rates plummeted and speculative bubbles inflated the value of stock options.

A second factor contributing to the rise of CEO pay after the 1970s was the erosion of corporate governance, which ran alongside the general regulatory retreat. Institutional economists have long recognized the basic dilemma of the modern corporation, in which ownership is diffused by shareholding and control is captured by managers. The result, as Thomas Piketty concludes succinctly, is that “top managers by and large [have had] the power to set their own remuneration, in some cases without limit, and in many cases without any clear relation to their individual productivity.”

These problems worsened after the 1970s. This was an era marked by a lack of managerial accountability, insufficient or opaque corporate financial disclosure rules, and uneven oversight by corporate boards, auditors, shareholders, and an underfunded SEC. And it was an era punctuated by corporate scandals (Enron, Tyco, Adelphia, WorldCom), which underscored and illustrated these pervasive problems. The Sarbanes-Oxley Act (2002) beefed up regulatory standards, but could not undo the damage or its lingering consequences.

At the root of this is the limited voice of shareholders. The implicit check-and-balance provided by professional managers on one hand and shareholders on the other has almost completely collapsed. The share of firms organized as public corporations is falling as private equity alternatives to the stock market proliferate. Increasingly, shareholding is dominated by the block holdings of big institutional investors (mutual funds, pension funds, and the like). And many public firms use “dual class” shares to distribute voting rights more narrowly than stock ownership.

Nowhere is the weakness of shareholders more evident than on the issue of CEO pay. Since 1986, the SEC and IRS have capped the deduction (at $1 million) that firms can claim for executive pay that is not “performance-based.” Performance-based pay, in turn, is subject to shareholder approval. But, in most instances, shareholders have to rely on the firm’s own description of its payment plan and its performance standards. And most firms have proven remarkably unconcerned about the rule, taking the deduction when they can get it but also increasing compensation even if they can’t write it off. The Dodd-Frank reforms (2010) gave shareholders slightly more oversight over the recommendations of corporate boards, with a new provision allowing them to “say no on pay.” But the shareholder vote is purely advisory, and has checked executive pay only in rare instances where a resounding “no” vote has been accompanied by public outrage.

The problem here is not just that shareholders have little opportunity or power to influence executive pay but that the excesses of those pay packages are effectively obscured or hidden. In this respect, the use of stock options and retirement packages to bolster executive pay is not just a tax dodge, but a concerted effort to camouflage the level and terms of executive pay packages with various forms of stealth compensation (such as lavish retirement deals) or rigged performance measures (such as stock options). Indeed, recent research suggests that executive compensation is not just indifferent to firm performance—dramatic failures can be quite lucrative—but potentially damaging, as lavish severance deals and stock options create incentives to skim the firm in the short run rather than build value in the long run.

In effect—with very limited input from shareholders and no demonstrable connection to firm performance—top executives set their own salaries. Most firms rely on nominally independent consultants or compensation committees to set the pay of top executives. But this advice comes from a closed circle in which directors serve on each other’s compensation committees, or in which the consultants that advise on executive pay are bidding on other contracts with the same firms. (For an incisive assessment of corporate boards, see the Center for Economic and Policy Research’s Director Watch project.) In 2006, for example, nearly half of the Fortune 250 companies contracted for compensation advice from consultants providing other services to the company—and there was a clear correlation between CEO pay and the extent of a consultant’s conflict of interest.

These compensation committees, in turn, have perfected a machine for ratcheting up executive pay. As a general rule, CEO pay is calculated from a benchmark of peers. The result is a lucrative game of leapfrog. The selection of peers is arbitrary—and often consists of cherry-picking larger and successful firms with higher paid executives. Since all firms proceed from the assumption that their executives are above average (the “Lake Wobegon effect”), the aim is then to best the median of the peer group—a practice guaranteed to ratchet up pay regardless of firm performance. Indeed, companies that employ compensation consultants end up paying their executives more and disguising more of that compensation in stock options and retirement deals.

Executive Pay and American Inequality

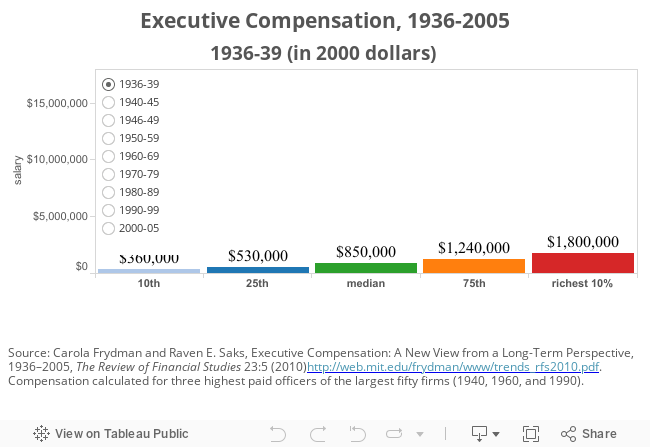

The link to rising inequality is clear. Going back to the 1930s [see graphic below], compensation for the median and the richest executives was relatively modest. Neither grew much into the late 1970s, but after that executive compensation took off—especially for the richest 10 percent. The trajectory varies a little, depending on whether stock options are counted when they are granted or when they are cashed in, but is startlingly steep by either measure. Between 1965 and 2000, CEO compensation (in real, inflation-adjusted dollars) grew by about 2500 percent. Compensation fell off a little during recessions of 2001 and 2007 but still vastly outpaced the growth of both average worker compensation (which inched up only about 30 percent from 1965 to 2011) and stock values (which a little more than doubled).

The starkest contrast—both as an index of corporate priorities and as a rough marker of inequality—is the growing gap between the compensation of CEOs and the compensation of the average worker. In the 1960s, the average salary for a CEO of a major U.S. company was just under twenty times the salary of the average worker [see graphic below]. By 2000, this had swollen to more than 400 times, and—by 2007—the median S&P 500 CEO earned in three hours what a minimum-wage worker pulled down in a year). As of 2012, the ratio of CEO-to-worker compensation (measured by options-granted) sits at just over 200 to 1. The disparity is particularly stark in corners of the economy where workers are battling for a living wage. Across the fifty largest low-wage employers, CEO pay is about 650 times the pay of a full-time worker. In fast food, according to a new study from Demos, CEO pay runs more than 1,200 the pay of the average worker.

All of this has had a significant impact on inequality, particularly on the growing gap between top earners and everyone else. Executives and managers (including in finance) make up about half of the top 1 percent and almost two-thirds of the top 0.1 percent. This group accounted for over half of the growth in income enjoyed by the top 1 percent from 1979 to 2005, and over two-thirds of the growth in income enjoyed by the richest 0.1 percent over the same span.

Inequality is also sustained by the tax treatment of executive pay. In 2010 and 2011, fully a quarter of America’s one hundred highest-paid corporate chief executives took home more in CEO pay than their company paid in federal income taxes. Tax liability is limited (or evaded) by the toothlessness of “performance-based” provisions in the tax code, by the loopholes surrounding stock options and deferred compensation, by the absurdly low capital gains rate, and by the various dodges that allow income to be repackaged as capital gains. The issue here is not just how little restraint the tax code has on very high incomes, but how little revenue—essential to the public programs and public goods that can redress inequality—is realized.

Changes in corporate governance, including transparency and real opportunities for shareholder input, could align executive pay more closely with performance and narrow the often grotesque gap between top executives and ordinary workers. More broadly, one would hope that this would yield not just a meaningful cap on executive pay, but a commitment to a fairer distribution of corporate earnings. Empowered shareholders, including those representing “workers’ capital” (pensions) might not only restrain executive excess, but also vote their values—making themselves heard on everything from the firm’s wage structure to its political positions.

Executive Pay in International Perspective

Here, again, the American circumstances are starkly at odds with those of its peers. In most of the rest of the OECD, corporate law and corporate governance is shaped by a much clearer sense of social and fiduciary obligation. Labor and shareholder representation on corporate boards is routine—in some settings even required by law. And, outside the United States, corporate regulation is national in scope—avoiding the state-by-state “race to the bottom” that marks corporate law in the United States.

While detailed international comparisons of executive pay are hard to make (given the variation in firm structure and compensation practices), the consequences are unsurprising. In the absence of the regulatory standards and social norms that limit executive pay in most other settings, the United States is a stark outlier [see graphic above]. By the widely used Tower-Perrin measure of “typical” or competitive compensation, American CEOs take home nearly double the salary of their peers in the next most lucrative setting, and more than triple the salary of their peers in most other settings. By a more conservative measure (using a smaller set of fourteen countries with mandatory pay disclosures), American CEOs still come out ahead—leading the pack on median compensation and trailing only Swiss CEOs on mean (average) compensation.

Executive pay has risen in the last generation not because there is a new premium on skill or results, but because the political currents that eroded the bargaining power of ordinary Americans have also buoyed the incentive and the opportunity of the richest 1 percent to pad their incomes. This has had a cascading effect on the structure of American inequality, widening the income gap between the richest 5 or 10 percent and everyone else, and widening gaps within the top 5 or 10 percent—as the very rich (the top 1 or 0.1 percent) hoard most of those gains. This is both a market malfunction and a democratic disaster, as the skewed distribution of economic rewards—in the wake of Citizens United and McCutcheon—is replicated and reflected in political resources.

Colin Gordon is a professor of history at the University of Iowa. He writes widely on the history of American public policy and is the author, most recently, of Growing Apart: A Political History of American Inequality.