Them That Has, Gets

Them That Has, Gets

There is no starker measure of inequality in the United States than net wealth—and over the last four years, the divide has only grown.

There is no starker measure of the United States’ growing inequality than net wealth—a metric that captures not just the accumulation of income inequality over time, but the deep sedimentary advantages of inherited wealth as well. Since 1962, the top 10 percent’s share of income has grown from 36 percent to 47 percent; over that same span, the top 10 percent’s share of wealth has hovered around 70 percent. In 2016, according to the latest Survey of Consumer Finances (SCF), the top 10 percent claims 77 percent of U.S. wealth. And about half of that, 38.5 percent in 2016, is claimed by the top 1 percent alone.

The new SCF documents substantial gains since the 2013 survey, driven largely by post-recession recovery of housing equity and stock values. But those gains, unsurprisingly, are hoarded at the top. The median net worth of the poorest 25 percent grew from less than $50 in 2013 (many of the poorest 25 percent have no or negative net worth) to about $200 in 2016. The median net worth of richest 10 percent grew from $1.93 million in 2013 to $2.4 million in 2016.

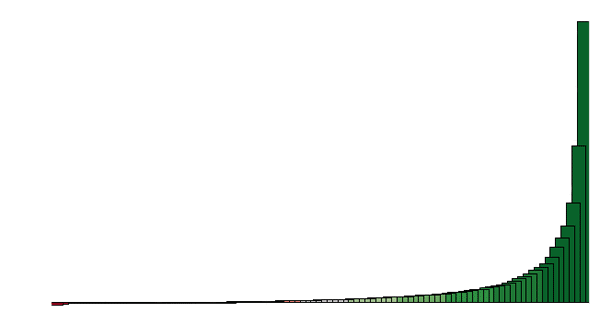

The graphic below charts the dizzying trajectory of wealth inequality, from 1962 to 2016. (The triennial SCF starts in 1983; this series, maintained by the Urban Institute, uses two one-off surveys—1962 and 1963—to extend coverage back another two decades).

In 1963, the bottom 1 percent was about $6500 in debt, the bottom 10 percent were barely breaking even, and the median household claimed a net worth of just over $41,000. By 2016, the debt burden for the bottom 1 percent was over $80,000, the bottom 10 percent were under water by about $1000, and wealth at the median had doubled to just over $97,000. At the top, that half-century was considerably kinder. The wealth of top 10 percent grew fivefold, from about $239,000 to over $1.18 million; the wealth of the top 1 percent ballooned more than sevenfold—to over $10 million in 2016.

These numbers are especially sobering, of course, because the tax plan winding its way through Congress would make things much worse. As currently drafted, the GOP tax bill would cuts rates on higher brackets, broaden exemptions from the estate tax, and further subsidize and encourage financialization. Rather than slowing down these mechanisms of wealth inequality, we are poised to grease their wheels.

Colin Gordon is a professor of history at the University of Iowa. He writes widely on the history of American public policy and is the author, most recently, of Growing Apart: A Political History of American Inequality.