Red Lines, Black Lives

Red Lines, Black Lives

A new digital archive reveals the extent of the federal government’s role in fueling and enforcing midcentury housing discrimination.

When Ta-Nehisi Coates’s made his influential “Case for Reparations” in the pages of the Atlantic in 2014, his focus, perhaps surprisingly, was not on slavery. It was on housing discrimination—all of the measures that, from the 1870s on, prevented former slaves and their descendants from getting their “forty acres and a mule,” from owning land and building wealth. While rooted in Jim Crow and the lost promise of Reconstruction, this disadvantage fully flowered in the middle years of the twentieth century—an era in which federal programs opened new opportunities for white families, but allowed the southern Congressional veto and local discrimination in both North and South to shut out most black families. It was an era, as Ira Katznelson and others have shown, “when affirmative action was white.”

A new resource hosted by the Digital Scholarship Lab at the University of Richmond reveals the extent of the government’s role in fueling and enforcing midcentury housing discrimination. In the 1930s, the New Deal’s Home Owners’ Loan Corporation (HOLC) financed or refinanced nearly one in every five residential mortgages in the United States. The HOLC, aimed at relieving distressed borrowers and lenders alike, revolutionized home finance and home ownership by offering long-term, low-down-payment options at a time when the standard commercial loan expected 50 percent down at sale and a payoff in three to five years. This intervention (and infusion) steadied banking and construction sectors rocked by the Depression. And, by dramatically changing the terms of home finance, the HOLC put homeownership within reach of much of the working class. Between 1930 and 1960, the homeownership rate grew from 48 to 62 percent.

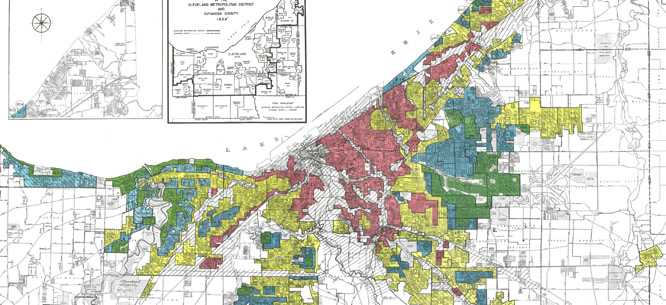

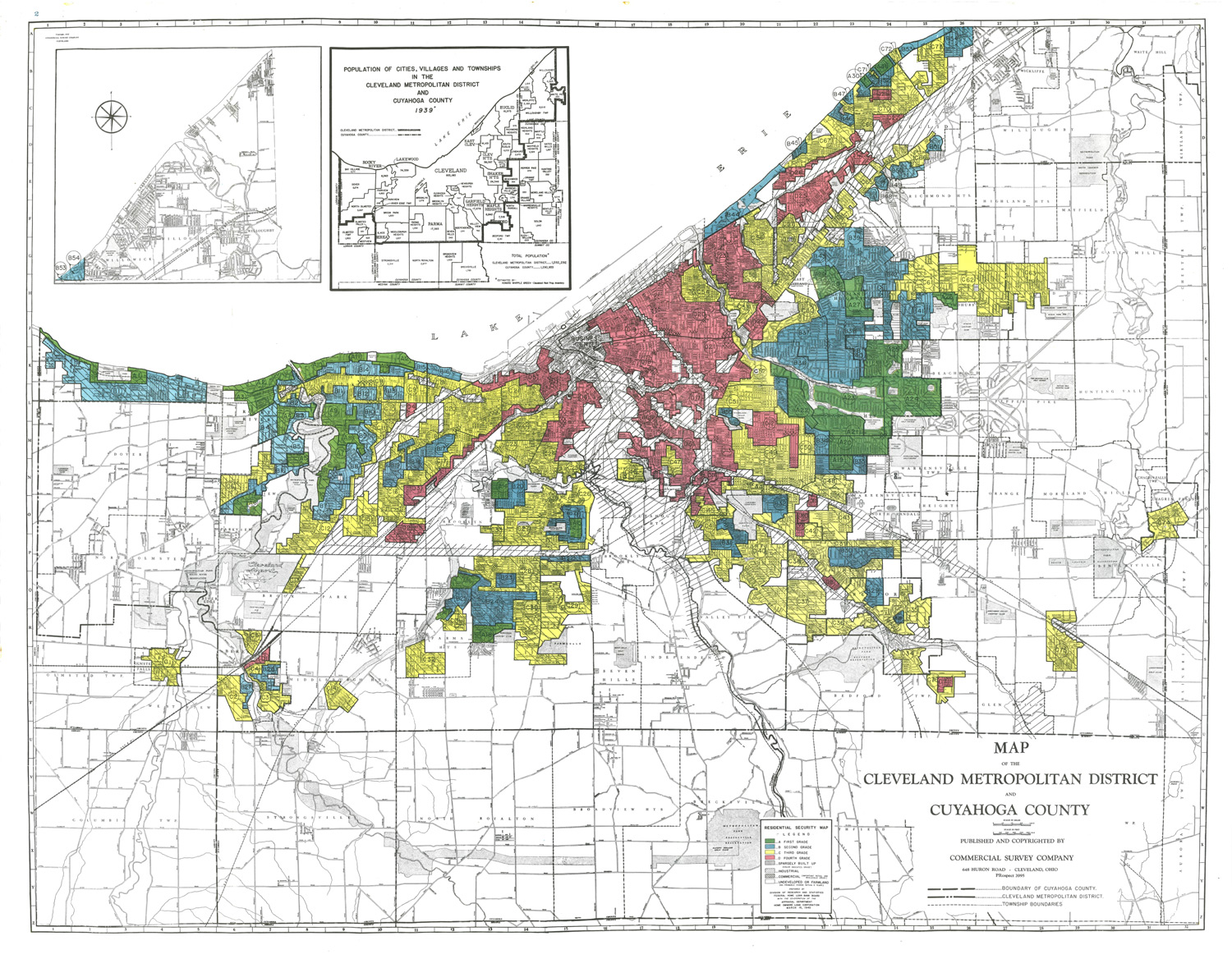

But the benefits, notoriously, were far from even. HOLC lending was guided by a hastily assembled library of “residential security” maps which rated the creditworthiness of virtually every urban neighborhood in the country. Lacking the capacity to survey cities themselves, the New Deal turned to local real-estate and finance interests whose first principle and guiding motive was the maintenance of racial segregation. The textual area descriptions which accompanied the HOLC maps echoed private real-estate appraisals of the era, which used the threat of racial “incursion” or “invasion” as the primary marker of property value and leaned on the strength (or weakness) of local restrictions such as race-restrictive deed covenants. In other words, the maps became the basis for three decades’ worth of relentless, federally endorsed redlining.

Following the lead of Kenneth Jackson’s Crabgrass Frontier (1985), a generation of scholarship has documented the motives and the impact of the HOLC’s redlining practices in particular settings. Now, a team of scholars working with the Digital Scholarship Lab at the University of Richmond has made the entire corpus of HOLC maps—and the accompanying area descriptions—accessible. The resulting database, Mapping Inequality: Redlining in New Deal America, is a remarkable accomplishment of publicly engaged scholarship. Geo-referenced on a national map, the 150-odd city maps offer a damning overview of the relentless scope of federal support for local segregation. Each city map in turn allows users to browse the area descriptions, which catalogued detrimental influences such as “colored population” or “absence of restrictions.” This was the fruit, as Robert Weaver (who would later serve as the first Secretary of Housing and Urban Development under Lyndon Johnson) noted bitterly in 1948, of turning a federal program “over to the real estate and home finance boys.”

In some respects, the maps presented here overstate the impact of the HOLC. Perhaps best understood as an inventory of existing practice in real estate and home finance, the HOLC did not invent redlining—indeed, as Jim Greer and others have suggested, it is unclear how just how widely used or distributed the maps were. What’s more, as Todd Michney and Amy Hillier have shown for a number of cities, the HOLC “red zones” that so often accompanied African-American occupancy did not preclude federal mortgage underwriting in those neighborhoods—although they did worsen its terms. In this sense, the HOLC maps succored subprime lending as much as direct disinvestment.

But in other respects, this presentation of the HOLC maps probably understates their impact. Alongside the easy equation of race and credit risk in established neighborhoods, the HOLC (and its parent agency the Federal Housing Administration) flooded the suburbs with subsidies for developers who—building cul-de-sacs in the cornfields outside St. Louis or Chicago or Des Moines—could easily meet federal guidelines for home size, lot size, setback and the like. These developments, many of which were “protected” by race-restrictive deed covenants before the soil was turned, were closed to African Americans. In this sense, the Federal Housing Administration discouraged investment in older city neighborhoods not by prohibiting it, but simply by ensuring that it was easier and more lucrative elsewhere.

Even if the HOLC just inventoried and codified what realtors and banks and developers were already doing, it had a profound impact nevertheless. Our expectation of public (especially federal) programs is that they will bring with them a commitment to equal protection—an argument made consistently, if not always successfully, with the growing scope of federal contracts, subsidies, social policies, and labor standards after the 1930s. But in housing, the federal government was not just timid in confronting racial segregation; it actively encouraged, subsidized, and sanctified it. It was as if the federal government decided to monitor voting registration in Mississippi in 1963, and outsourced the job to the local Klan.

By laundering housing policy through the systematic and candid racism of local real-estate and finance interest, the HOLC also opened a gap between black and white ownership that has never closed. In the new world of home finance, white families bought homes at higher rates, they bought them earlier in life, they bought them on better terms, and they bought them in neighborhoods where housing value appreciated reliably. This yielded, of course, a widening of the racial wealth gap even as other disparities (wages, income) closed slowly in the civil rights era and after. Today, median African-American family wealth is less than one-tenth that of white families—a gap largely attributable to disparate access to housing subsides such as the HOLC, and their impact across generations.

In turn, this segregation and stratification of opportunity have hardened the inequalities that—especially in the American context—flow from housing. Declining or stagnant home values sap the funding of local services, especially schools, that rely on local property taxes. Our public policies in the last half century made it hard for African Americans to escape central cities but easy or natural for jobs to do so—resulting in an enduring mismatch between residential and economic opportunities. And the “neighborhood effects” of segregation and concentrated poverty are pernicious and persistent across a range of social and individual outcomes—including public health, cognitive ability, social mobility, and civic engagement.

The HOLC maps collected at Mapping Inequality provide much more than an accessible archive of a sordid moment in the history of American public policy—although that alone would be worth the price of admission. They document the motives and scale of discriminatory practices that have always animated the American real-estate industry (“just one of those things” that everyone was doing, as Donald Trump lamely offered in defense of his own history of racial bias), and which persist to the present. And they shine a light into the long shadow of systematic housing segregation and discrimination whose consequences—in neighborhoods, and in the opportunities that one generation can offer to the next—are unabated.

Colin Gordon is a professor of history at the University of Iowa. He is the author of Mapping Decline: St. Louis and the Fate of the American City (2008) and a companion website.